One of the most compelling storylines of the election is whether Republican candidate Donald Trump can make good on his promise to make America’s economy great again. A review of his economic plan shows this is wishful thinking if Trump’s current ideas become American fiscal policy.

The focus of Trump’s plan is growing the American economy by deregulating, shifting trade policy and slashing taxes. In a recent speech at the Economic Club of New York, Trump vowed to cut taxes by a total of $4.4 trillion by lowering the top individual rate to 33% from 39.6% along with raising the standard deduction to close tax loopholes (Reuters). Trump claims his plan would not add to the federal deficit. To help compensate for the tax cuts, he would use a “Penny Plan” that would shrink all government programs outside of defense and entitlement programs by 1% each year (Reuters).

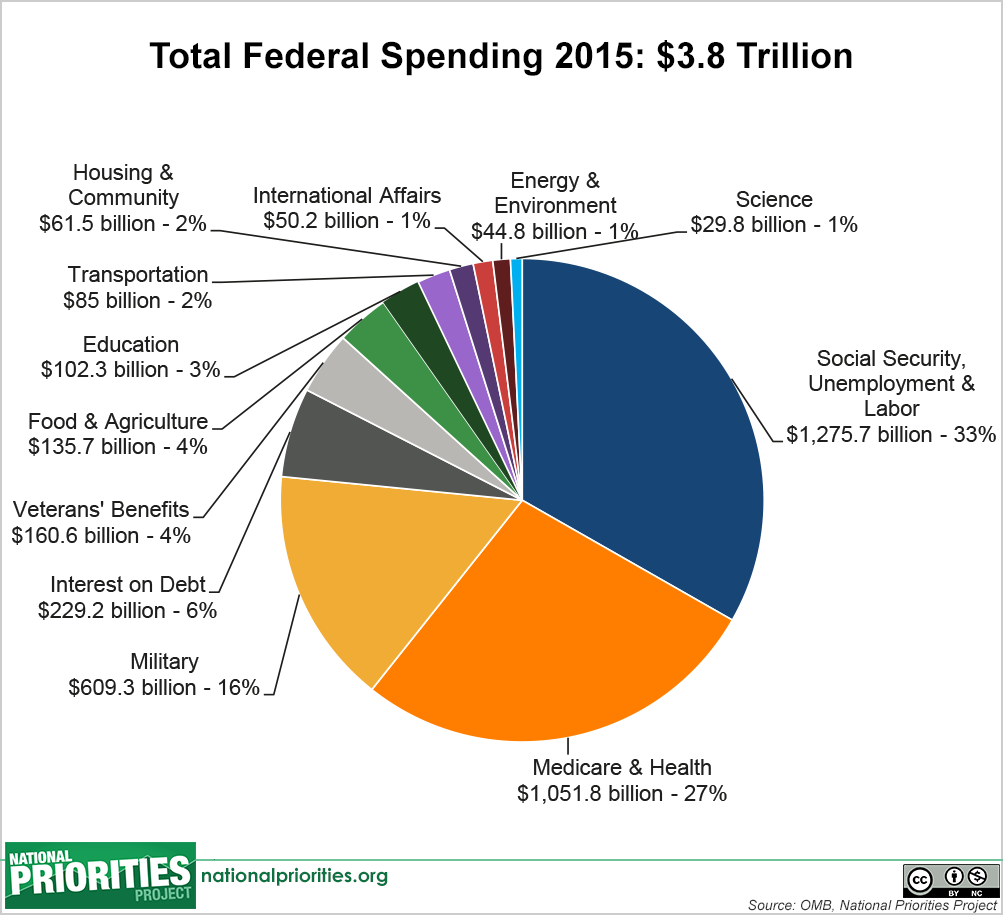

Trump claims the tax cuts would stimulate consumer spending. More realistically, the tax cuts would result in a deficit. The 2015 Fiscal Budget spent about $2.94 trillion of its $3.8 trillion on entitlement and military spending that would not be touchable under Trump’s plan (National Priorities). If 1% of the remaining $860 billion was cut, it would result in a $8.6 billion decrease in spending. This is a fraction of what Trump would need to fund his tax cuts. This means he will either not be able to execute planned government projects, such as his infamous wall, or incur a huge deficit.

From his sweeping immigration reform to his “Americanist” economic policy, Trump’s overall campaign has had an isolationist theme. Combined, they could have a drastic effect on the global economy. Trump plans on making net trade a positive part of the GDP by renegotiating or eliminating trade agreements such as NAFTA and the not-yet ratified Trans Pacific Partnership (CNN Money). This would include high tariffs on major trade partners such as China and Mexico, two of Trump’s favorite bogeymen. Trump promises to make up for lost imports with American products, saying, “We are going to put American steel and aluminum back into the backbone of our country.” (Time)

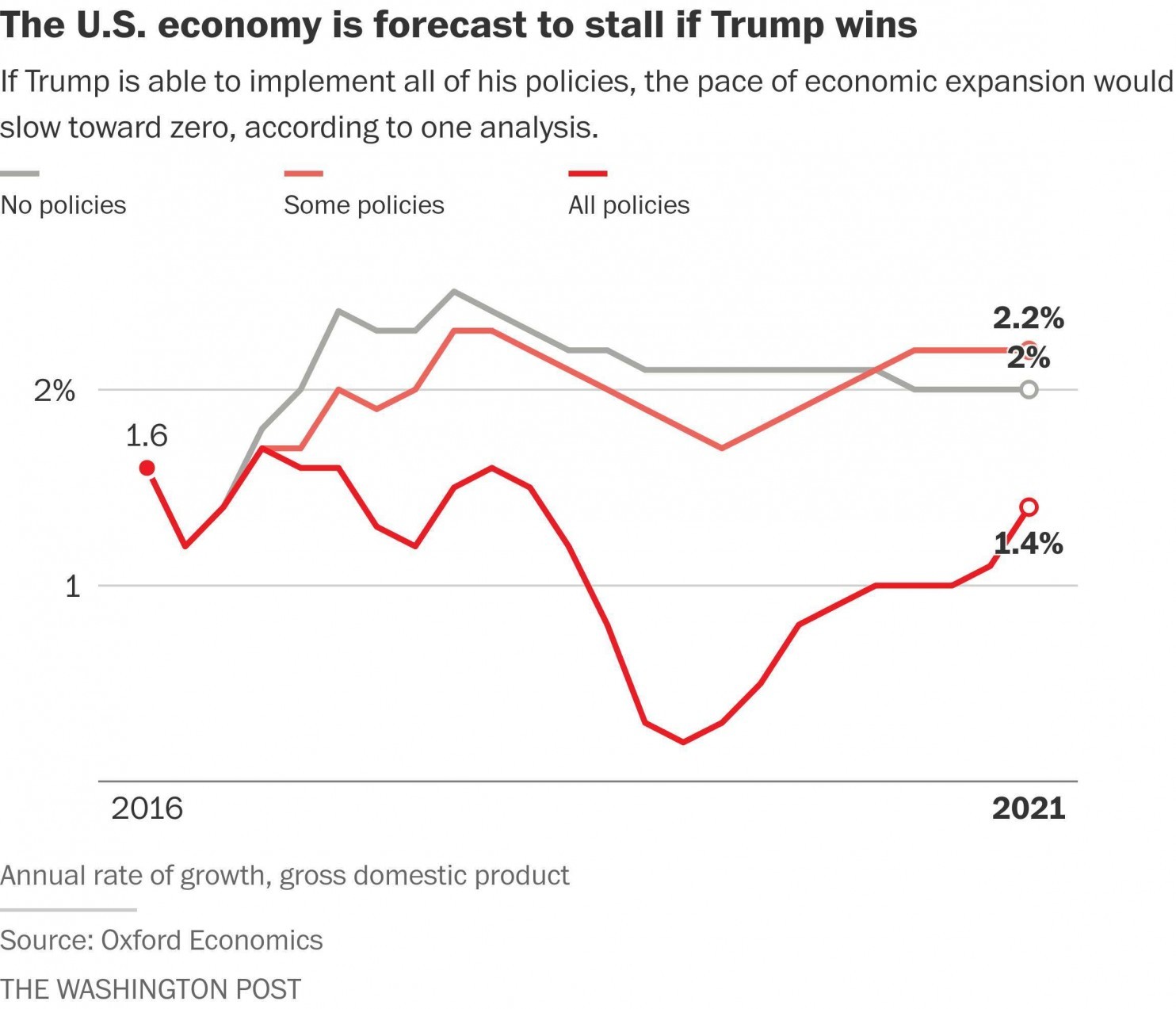

Trump predicts that his economic plan would result in a growth rate of 3.5% and create 25 million American jobs (CNN Money). These figures sound too good to be true, most likely because they are. Analyses by Oxford Economics and The University of Pennsylvania’s Wharton Budget Model estimate Trump’s policies would result in 4 million jobs lost, sharp declines in consumer spending, a global trade war and a total loss of $1 trillion in U.S. GDP by 2021 (CNN Money). His economic advisors have brushed off criticisms of his policies. “One thing we know about economists is that they never get it right,” said Trump economic advisor David Barrack (CNN Money).

In this case, the economists are right. If Donald Trump influences the U.S. economy, America will take a huge leap backwards. Trump’s plans to increase domestic manufacturing are not compatible with today’s global economy. Many of the parts in Mexican and Chinese goods originate in America. For example, Rich Turner and his 2700 worker denim plant in South Carolina would be out of business because they send most of their denim to Mexico to be sewed into jeans (CNN Money). Trade with Mexico and China helps all parties. Donald Trump’s misunderstanding of today’s economy could make America the opposite of great if he is elected.

Works Cited

http://www.reuters.com/article/us-usa-election-trump-economy-idUSKCN11L27G

http://money.cnn.com/2016/09/14/news/economy/donald-trump-economic-plan-1-trillion/

http://time.com/4386335/donald-trump-trade-speech-transcript/

https://www.nationalpriorities.org/budget-basics/federal-budget-101/spending/