For a sport that’s only been around for 10 years or less, competitive gaming is already turning into a lucrative field.

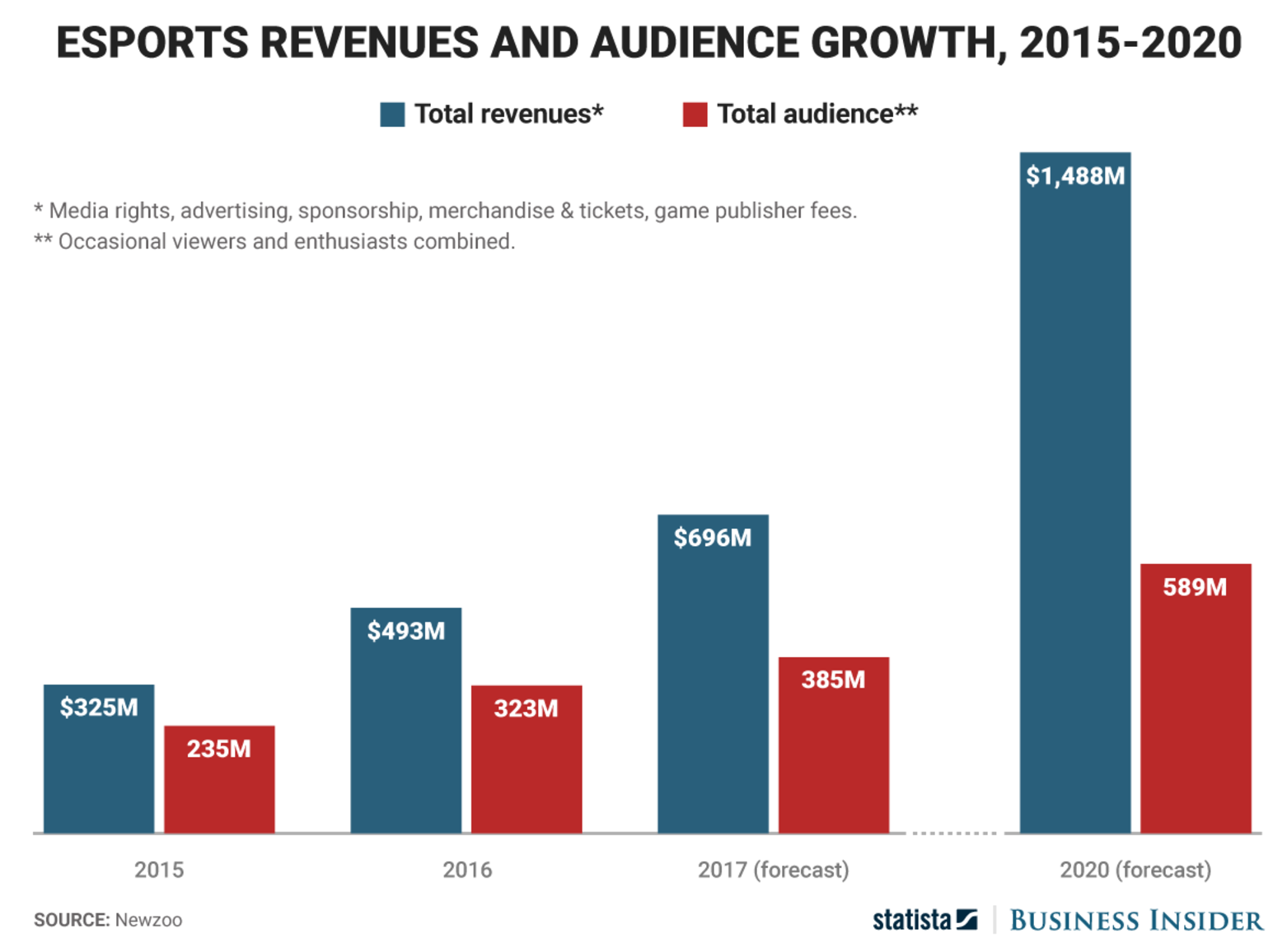

A Business Insider report released in March of this year shows that $800 million will be made on eSports in 2020. That doesn’t include media broadcasting rights, which, if included, are estimated at $1.5 billion.

This year eSports raked in about $700 million and Goldman Sachs has it growing at 22% per year.

For comparison, the National Football League made about $13 billion in the 2015-2016 season. That’s roughly 13 times more than what eSports is making now, but it’s hard to compare eSports to the NFL because it isn’t as much of an established brand.

This year, eSports has about 400 million viewers. Last year, the NFL had about 18 million views per game during the regular season, which adds up to 4.3 billion viewers.

But the NFL has seen a drop in viewers over the past couple of years, while eSports has seen a steady increase. The purpose of comparing these two sports helps add context to the numbers. Even though eSports is growing it won’t take over NFL viewership anytime soon.

You may ask yourself, how do people playing video games competitively generate millions in revenue? One, the popularity is immense. The finals for the popular game League of Legends sold out the Staples Center. Two, companies can sponsor players and teams which helps generate revenue. And finally, selling media licensing to broadcast games is very profitable, and will likely even be more profitable once media companies realize the sport’s popularity.

The majority of the people who consume eSports are young and view almost all content digitally. Getting advertisements to that demographic is no problem, but getting them to respond to it is another story.

A lot of companies are already looking at entering the space. Twitch, a platform primarily used for people to stream themselves playing video games but also used for eSports, was purchased by Amazon in 2014. ESPN has an eSports vertical on their site. YouTube has their own gaming section.

There are unique ways that eSports can be monetized so it will be interesting to see how this medium will grow in the future.