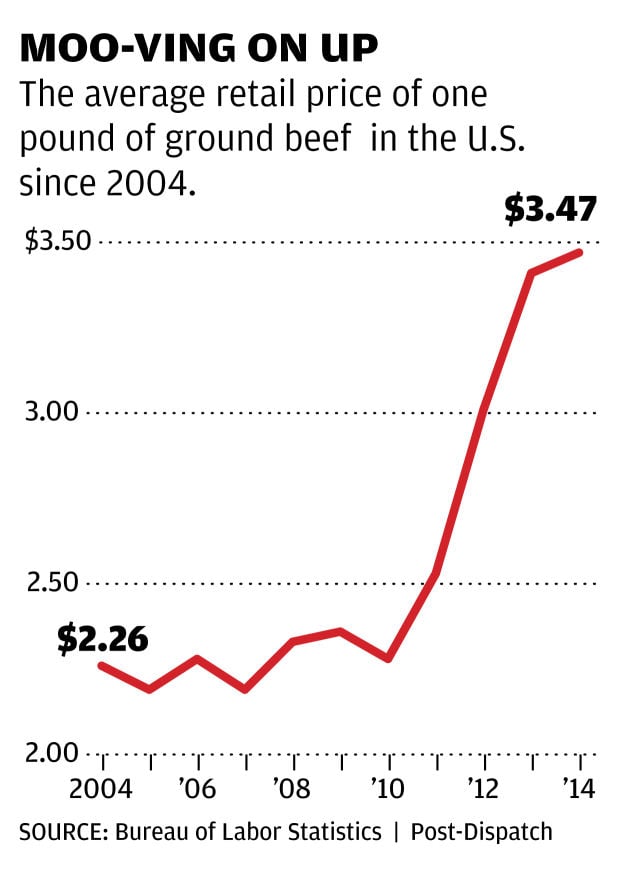

Maybe you haven’t noticed a change to the offerings at your family dinner table or the prices at your favorite restaurant, but meat prices have skyrocketed recently mainly due to droughts in recent years in Texas, America’s biggest state for cattle. Experts have cited the most devastating drought Texas ever saw in 2011, the driest year the state has experienced. But 2011 wasn’t the last of the drought, as Texas has experienced several other less severe droughts since as well as the rest of the southwest region. When adjusted for inflation, the price per pound for ground beef has hit $3.55, a 56% increase from just 2010. This drastic weather has dramatic reprecussions that all of America is now facing.

What this drought means is that feed prices have gone through the roof, which in turn means that cattle ranchers are now forced to raise fewer cows. So, less cows being raised, that surely isn’t enough to see the highest prices for beef in 30 years is it? But there are more problems causing these prices increases, mainly due to emerging countries and economies like China who are now eating more beef. Meaning, the decrease in product (cattle) is corresponded with new, emerging economies. David Anderson, an agricultural economics teacher at the University of Texas A&M explains the surge in demand for emerging economies like China “One of the things that happens that we see in people everywhere: When their incomes go up the first thing they do is they upgrade their diets, and so that usually means eating more meat.”

When you look at all of these factors in play, it’s a simple equation of a shrinking supply, higher demand, translating into record-level beef prices. But it’s not just beef that is seeing prices climb, according to CNN all other cow products like eggs, milk, and butter are being effected as well.

With the grilling and barbecuing season about to begin, you might be seeing more chicken, pork, or fish instead of those tasty cuts of beef, as it looks like these record prices are here for the longterm. Experts are predicting that high demand overseas will stay at a constant, so unless California, Texas, and the southwest region see some unexpected summer rain, be careful before selecting your protein.

Sources: http://www.npr.org/blogs/thesalt/2014/04/14/302858835/drought-increased-demand-contribute-to-high-beef-prices

http://money.cnn.com/2014/04/14/news/economy/beef-prices/