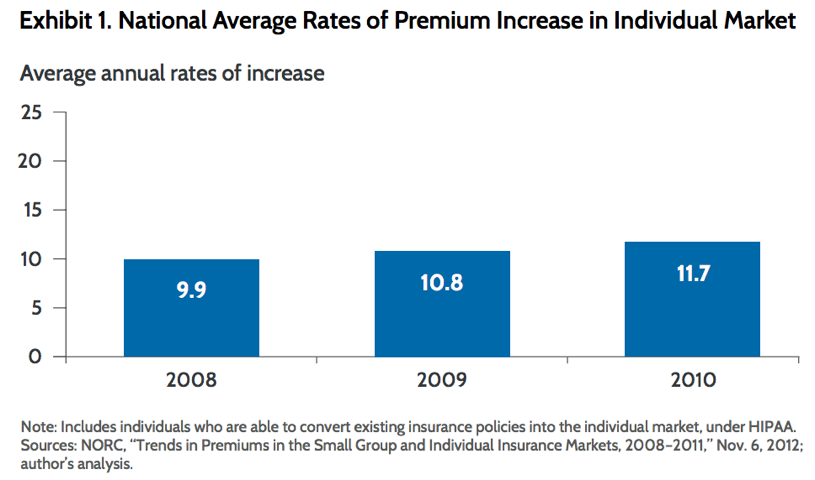

Disrupting America’s existing healthcare system was not going to be easy, but President Obama centered his legacy legislation around the effort. According to the Commonwealth Fund, “The Affordable Care Act (ACA) represents the most fundamental change to the structure of U.S. insurance markets in decades.” The disruption was a long time coming and the need for charge originally stemmed from many problems, but most notably, rising healthcare premiums. Please see the data below from The Commonwealth Fund which exhibits the rise in premiums over just 3 years:

Something needed to change and President Obama saw this market failure as an opportunity for intervention. When introducing the bill, President Obama articulated the reasons why the change was necessary at a speech in Maryland. He stated, “I knew that if we didn’t do something about our unfair and inefficient health care system, it would keep driving up our deficits, it would keep burdening our businesses, it would keep hurting our families, and it would keep holding back economic growth.” Fast forward to 2017. Looking at the healthcare system before the implementation of the Affordable Care Act, and now 7 years later in 2017, there have been notable market effects that are worth looking into.

First, the Affordable Care Act introduced more patients into the healthcare market by expanding insurance to more people. Health Affairs summarized the way The Affordable Care Act expanded health insurance in three ways: “the expansion of Medicaid to cover the poorest segment of the population (those with annual incomes below 138 percent of the federal poverty level), health insurance subsidies on the new exchanges for low- and medium-income people (those with annual incomes of 100–400 percent of poverty) who lack access to employer coverage or Medicaid, and a mandate for the uninsured to buy coverage.” When there are more people in the market, subsequently there is more business for the market. According to an article The New York Times published just one year after the Affordable Care Act became law, it reported that the stock market actually performed quite well for hospitals, drug companies and for-profit health insurers and that “the S&P 500 Health Care Index rose by 24 percent over the last year, outperforming the overall stock market.”

However, with a growing pool of healthcare recipients, greater risk is inevitable. Before the Affordable Care Act, people with pre-existing conditions who did not have access to insurance from the government or their employers, did not have many options for gaining healthcare coverage. Now, those high-risk patients are qualified for insurance coverage under the law and put on an equal playing field with healthy patients. Although more people are getting coverage, the new people being introduced into the pool are mostly poorer, sicker people. The Kaiser Family Foundation looked deeper into how the addition of higher-risk people would fluctuate the existing premiums. “Prohibiting discrimination against people with pre-existing health conditions will tend to raise premiums as higher cost individuals who have previously been excluded from the market buy coverage,” Kaiser concluded but eased worry with the fact that “this may be offset by an influx of younger and healthier people, due to the ACA’s individual mandate and premium subsidies for low- and middle-income people buying insurance in new health insurance marketplaces (also known as exchanges).”

Secondly, not only has more risk entered the market, but new economic restrictions have been placed on the insurance industry. With more people and more insurance companies, competition within the market is heightened. The Supreme Court ruled in 2012 that states had the opportunity to opt of the Affordable Care Act’s Medicaid expansion. As a result, some state governments now have differing policies and rules for the insurance market. According to Kaiser, insurers are being more closely monitored by not only the federal government, but some individual state governments, including a cap on how much those insurers can make from coverage of individuals. Not only are insurers being restricted, but hospitals are as well. The New York Times reports that “hospitals are being hurt by a provision of the law that cuts their Medicare payments by $260 billion over 10 years, but they have benefited from having more insured customers who can pay their bills.”

So it seems the healthcare market has a way of naturally balancing what seem to be significant effects on its existing market, but of course with change, there are always winners and losers. So who is suffering the most for the greater good of all Americans? The answer: Middle class, healthy Americans who already had health insurance before the Affordable Care Act became law. Yahoo Finance reported people who have already purchased insurance plans, because they could afford it or qualified for the existing coverage, had their coverage cancelled because it did not meet the new requirements by law of the Affordable Care Act. The market once again balanced out according to a study done by Health Affairs, concluding that most of the Americans who had to exchange their plans were probably going to switch anyway and were mostly likely getting a better a deal on their new plan than if they were to purchase it before the Affordable Care Act came into play.

Naturally, there are outliers in this situation. Brenda Laster, a 49-year-old self-employed, single mom of two living in Rogersville, Tennessee is one of the losers in this situation. She claims, “Blue Cross Blue Shield of Tennessee provided me with good coverage and access to good doctors and I didn’t want to switch. Now I am paying more for coverage and I don’t see a difference.” People like Brenda get the short end of the stick with the Affordable Care Act, but it seems as if it is a necessary evil to improve healthcare for all Americans in the future.

Kentucky has some similar cases as well. A spokesperson from the Majority Leader’s Office states that “middle class Kentuckians are hurt the most by the ACA because of the increasing costs. Because the costs keep rising, many of the healthy middle class individuals are leaving the market and paying the penalty instead.” This is bad for the middle class, but so many poor and sick Kentuckians, especially in the Appalachian region, are now getting access to insurance, which as mentioned before, is offset by the inclusion of younger, healthier people into the market. The healthy people are subsidizing the sick and those with pre-existing conditions, which is helping ease more people into the market, providing a way for the government to get involved and address some of the inherent problems President Obama mentioned earlier, without breaking their own bank.

On the opposite side of the spectrum, the sacrifice of some will pay off for our economy as a whole. The New York Times reported “the Department of Health and Human Services estimates that hospitals will save $5.7 billion in so-called uncompensated care costs this year because more people have insurance. And nearly three-quarters of those savings, $4.2 billion, has gone to the 25 states and the District of Columbia that expanded Medicaid at the beginning of 2014.” The temporary pain will be worth the long term gain for the healthcare market as a whole, because improvements have already been made. The New York Times also reported progress back in 2014 stating “the last few years have seen a significant slowdown in the growth of health spending. Across nearly every measure — medical price growth, employer insurance premiums, per capita Medicare spending — the amounts the country spends on health care have increased by much smaller margins than the nation is used to.” However, we have to take the decrease in health spending with a grain of salt. Kaiser conducted a study that found that “because GDP and inflation influence health spending with a significant lag, the effects of economic cycles on the health system are not always apparent from looking at such simple relationships.” This study is essentially saying it is possible the Affordable Care Act could not be the only reason for the decrease in health spending and that GDP, inflation and even global economic trends can also play a role in that decrease.

For most middle class Kentuckians and Brenda Lasters of the population, it seems unfair but the pros will outweigh the temporary cons in terms of the Affordable Care Act having a positive economic effect on the healthcare market. The implementation of the Affordable Care Act was always going to attract political controversy because change usually does, but from an economic perspective, the data supports a mostly positive impact on the economy as a whole. After 7 years of the Affordable Care Act being embedded in the economy, alterations to the law would have a significant impact on all Americans. CNN gathered research from the Congressional Budget Office estimating that “repealing Obamacare would increase Medicare spending by $802 billion over 10 years.” President Obama’s legacy legislation had the intent of disrupting the current economic market and disrupt it has. Current debate of removing the law and replacing it will have just as much of an economic impact as introducing the Affordable Care Act in the first place.

Leave a Reply

You must be logged in to post a comment.