Signed into law on April 5, 2012, the Jumpstart Our Business Startups (JOBS) Act aimed to energize startup businesses by leveling the investment playing field. By eliminating a number of the barriers that had previously prevented startups from formally seeking capital be selling equity, the investment game would, theoretically, become a more level playing field—no longer a realm solely inhabited by wealthy venture capitalists.

One problem, though.

The Securities Exchange Commission (SEC) has gotten through six of the seven titles in the JOBS Act, essentially removing all the barriers that had previously prevented startups from selling equity as a means of funding. However, the agency has been unsuccessful in giving individuals the most logical method of investing—funding portals. Consequently, the rest of the act remains in a holding pattern, waiting for potential investors to have a way to access these companies that are now able to seek funding in exchange for equity at any time.

Crowdfunding and Venture Capital

Spawned by the same so-called “collaborative economy” that produced a host of well-known peer-to-peer (P2P) businesses such as Uber and Airbnb, crowdfunding platforms are online portals that (as their name implies) enable startup companies or sole proprietors to seek funding from the masses. Aspiring entrepreneurs to set up pages to market their idea to the public in hopes that enough people want to contribute any amount of funding to help get it off the ground. The big-picture idea behind them is to democratize entrepreneurship by giving all startup businesses the same chance at raising funds, but strictly by donation. Those who contribute to the business venture get nothing in return.

Contrast that model with venture capital, in which these same aspiring entrepreneurs go straight to big money organizations that decide whether or not they will invest large sums in exchange for some measure of control over the company. VCs will own a significant percentage of the new company in exchange for funding, often times taking prominent seats on boards as another method of exercising ongoing control over day-to-day business operations. Of course, when one of their companies hits and goes public or is sold, VCs turn their shares into large sums of cash.

Background on the JOBS Act

Signed into law on April 5, 2012 (SEC), the Jumpstart Our Business Startups (JOBS) Act aims to promote economic growth by easing certain securities regulations and encouraging more funding of small businesses. As is usually the case with any sort of legislation, it led to legal wrangling and a stepped implementation that is still not complete today—more than three years after the act was initially signed. Titles I, V and VI essentially opened up new capital opportunities for job creators and were passed right away.

Titles II, III and IV—all of which involve crowdfunding in some way—have proven to be more problematic.

Title II, which was the first to allow early-stage companies to solicit investments without being listed publicly, went into effect September 23, 2013. Essentially, the SEC removed the gag order that previously prevented startup businesses from leveraging the capabilities of the digital age to broadcast to the masses that they’re looking for funding and could sell equity to get it. No longer do they need to be public companies.

Commonly known as Regulation A+, Title IV expanded Regulation A of the Securities Act of 1933 into two tiers: one for offerings up to $20 million over a 12-month period and one for offerings up to $50 million over a 12-month period. The SEC released its rules for Regulation A+ in March of this year, and the modified Regulation A became effective June 19, 2015. Essentially, a company’s funding goal no longer has to be so outrageous that it prices crowdfunding out of the question and requires VC money to participate.

Title III would enable crowdfunding platforms such as Kickstarter and Indiegogo (which the SEC refers to as funding portals) to become startups and equity crowdfunding, but it remains in a legislative quagmire (SEC Q&A).

Potential Impact on Startup Funding

While the JOBS Act has not yet seen all of the equity crowdfunding provisions come to fruition, two of the three major titles related to it are in practice today. Startup businesses are allowed to announce they are seeking funding and can raise up to $50 million in a calendar year from any investors—accredited or not.

From the investor’s standpoint, anyone now has the opportunity to purchase equity in any private company that makes it known they’re seeking funding. While they’d be doing so on a much smaller scale than that of traditional VCs, these individuals no longer face the requirement of making more than $200,000 of income of having $1 million in assets. In short, the entire process has (theoretically) been opened up to the 99 percent (Forbes).

Title/Party of Three

Many of the arguments the SEC was forced to navigate in approving Titles II and IV had to do with protecting investors, since they were altering or removing policies that had long been viewed as safeguards against bad investments. Legislators were skittish about removing the separation between small companies seeking funding and individuals who may or may not have known enough to make informed decisions about investing.

Perhaps paradoxically, Title III involves the funding portals that, in addition to being the enabling platforms behind these investment transactions, could also provide that sort of third-party guidance. Of course, they could also become de facto gatekeepers, deciding who “gets to” invest in certain companies. As the debate continues, the two most prominent potential funding portals watch from the sidelines, waiting to see what shakes out but with very different levels of interest.

Per an August article from gaming publication Polygon, Kickstarter expressed no plans to enter the equity crowdfunding fray. Indiegogo, however, has expressed interest since the SEC released its Regulation A+ rules early this year. While the two are direct competitors in “traditional” crowdfunding, Indiegogo positions itself as being broader in scope. Therefore, it is willing to be more aggressive in its methods for enabling entrepreneurship any way and anywhere.

![]()

“Indiegogo will have done its job when Silicon Valley is no longer perceived as the epicenter of entrepreneurship,” co-founder Danae Ringelmann said. “It’s not, and our job is simply to catalyze the entrepreneurial spirit that exists everywhere.”

The company is also more aspirational when it comes to this idea of democratizing funding. Ringelmann’s co-founder Slava Rubin didn’t shy away from the idea of leading the crowdfunding equity charge when reacting to the SEC’s Regulation A+ announcement last March (Fast Company).

“The balanced regulations announced yesterday will not only protect investors but allow anyone to invest in the ideas they believe in,” Rubin said. “Our mission at Indiegogo is to democratize finance, and we are continuing to explore how equity crowdfunding may play a role in our business model.” (Crowdfund Insider)

Unfortunately, until Title III finds its way into practice, Indiegogo’s vision for completely open, equity crowdfunding will remain solely aspirational.

Wider Economic Implications

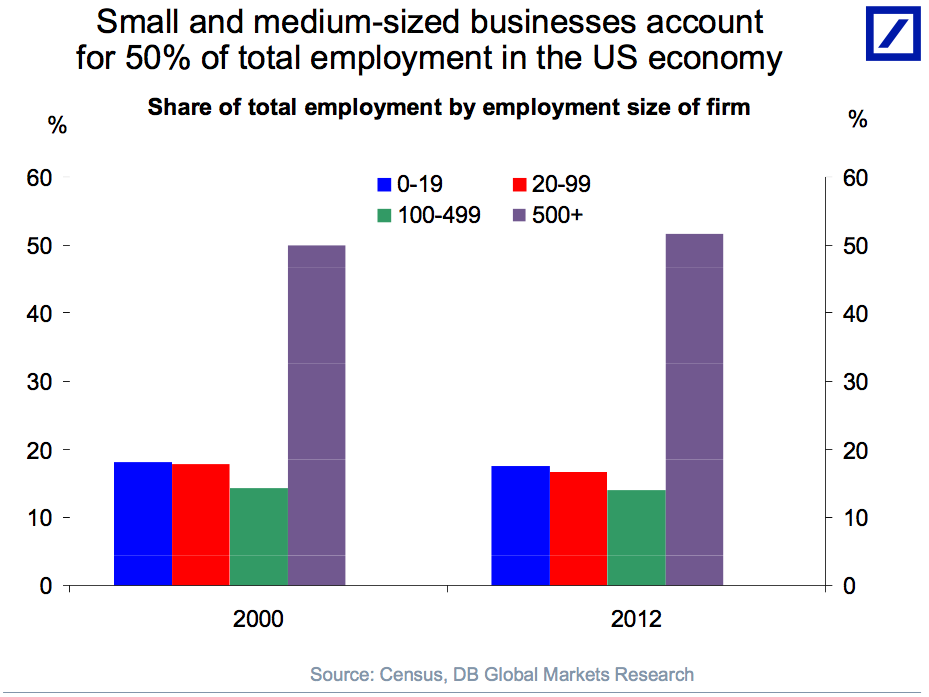

With the country only a few years removed from its worst financial crisis since the Great Depression and employment numbers still lagging, the JOBS Act passed through Congress with nearly full bipartisan support. Small businesses (defined as having fewer than 500 employees) accounted for half of all US employment in 2012 and were clearly seen as the key to continued economic recovery.

Locking half of the economy out of being able to draw on peers for funding doesn’t seem to make much sense when the goal is growth. Furthermore, when more than 70 percent of the country’s GDP is based on consumption, while investment accounts for a little over 10 percent, opening up more opportunities for people to invest their money seems like a no-brainer.

Additionally, with the Fed keeping interests at their current levels, spending and investing is exactly the type of activity the government is encouraging. Federal regulators want investment in small business because it’s leading the economic recovery.

Yet, the current implementation of the JOBS Act still doesn’t include the one piece that is likely to organize this more open investment environment into a viable alternative to the current, VC-driven establishment. But if it does come into practice, there appears to be a challenger on the horizon, brandishing a bright magenta logo and millions of potential investors.

The 99 percent is ready to change the game as soon as the SEC can get out of the way and let them. Same old, same old in the startup game…today.